Green energy loans are a fantastic way to finance energy-efficient upgrades.

We are big proponents of the cost-savings of upgrades like solar and heat pump hot water, but not everyone can afford the upfront investment. If someone is unable to afford the upfront investment, they can become stuck in a vicious circle of higher bills –> difficulty in saving –> can’t afford more efficient appliances –> higher bills etc.

Pleasingly, there are green energy loans on the market with ultra-cheap interest rates. Even people that can afford upgrades might be attracted to borrowing (if, for example, the green energy loan rate is lower that their mortgage rate).

Below, we discuss green energy loans with a clear message – there are some incredible deals out there!

Upgrades

I use the term “Green Energy Loans” broadly – I mean taking out a loan to fund a more efficient, electric house. This includes obvious examples like solar and heat pumps, but it can also include less obvious upgrades like insulation and double-glazed windows.

Let me illustrate with an example. Let’s say Pamela and John are looking to install a heat pump hot water unit for $2,000 to replace their old gas hot water unit. Pamela and John can either pay cash for the heat pump, or can borrow at an interest rate of 5% (green energy loan interest rates are typically lower than this, but I’ll keep it simple). Pamela and John’s interest repayments are going to be roughly $100 per year. But as we’ve illustrated in our case studies, Pamela and John with two people in their house can save upwards of $500 per year with their heat pump. Even though they are paying for the cost of finance ($100), they stand to be around $400 better off per year ($500 savings less $100 interest payments).

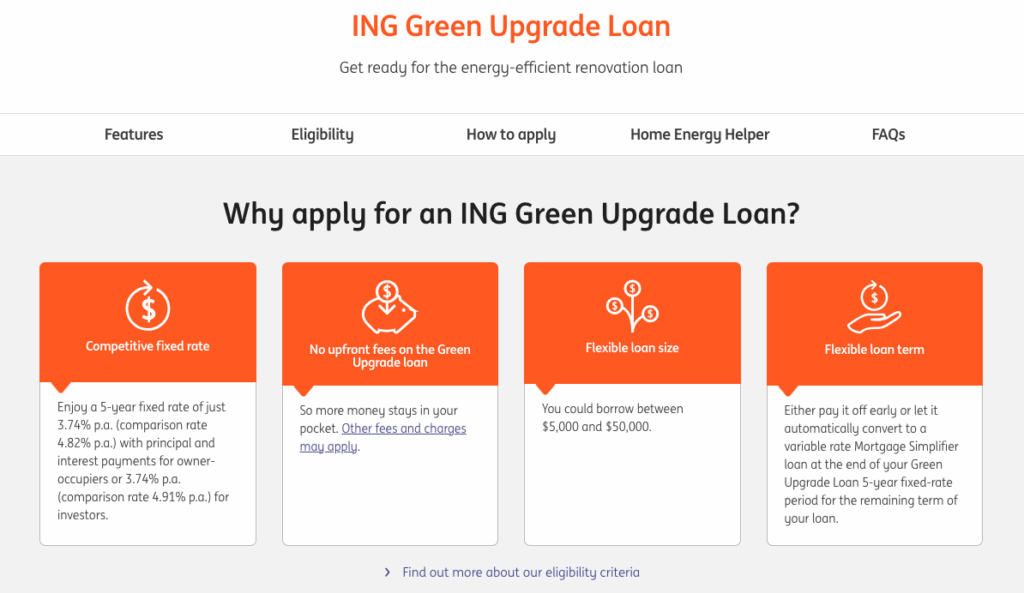

ING currently have Green Upgrade Loans available from as low as 3.74% (4.82% comparison rate for owner-occupiers). Conditions apply.

Loans are available for solar, battery, heat pump hot water, induction cooktop and certain air-conditioner installations.

ING is not the only provider of green energy loans. In fact a number of lenders have similar products. CBA has a 3.99% loan and Westpac has a 3.74% loan. Many customers might already use a bank that has a green upgrade loan special and there are general lenders for those whose bank doesn’t have a special.

Home Loans

Some lenders are offering discounted loans to those looking to refinance their home loans. ING offers $1,500 cash back to new refinancing customers that also install eligible energy-efficient upgrades. For existing customers, ING offers $500 cash back for those looking to refinance and perhaps take out a green upgrade loan.

I really like seeing this because large lenders, that know a thing or two about finance, are clearly seeing the value in energy efficient upgrades. They are in effect saying that if you carry out these upgrades, you will save money with lower energy bills and you’ll be a more attractive customer (or, in other words, a less risky customer). And they are willing to put their money where their mouth is. If the benefits are so very clear to them, they should be clear to us as well.

28Watt

We have been speaking with 28Watt, a company dedicated to finding customer’s the best green loans and mortgage rates. 28Watt’s Home Upgrades tool compares various lenders to find you the cheapest rate.

If you are interested in speaking with 28Watt, please feel free to use this form. This is a specific link showing you’ve come from Powrhouse, so they’ll look after you (and full disclosure, Powrhouse may receive a referral fee if you proceed with certain loans).

Too Good to be True

At first we might look at some of these ultra-cheap loan rates and wonder if they are too good to be true. The Clean Energy Finance Corporation (CEFC) is a large part of the reason for ultra cheap green energy loans. The CEFC is an Australian-Government owned green bank set up to help finance Australia’s clean energy transition. They have set aside $1bn in funding to offer discounted finance to customers through co-financiers to help increase housing-sector sustainability.

While some of the loan rates appear too good to be true, they are not. The CEFC’s funding is effectively subsidising the loan.

Is it “Interest-Free?”

We had a customer recently ask if we provided interest-free finance for a heat pump installation. I had heard of interest-free finance but I was immediately skeptical. Why would a lender offer a loan for zero interest?

I looked into offering interest-free finance to Powrhouse customers and discovered that while the loans are interest-free, they are marked up. Instead of charging the customer, the lenders charge the merchant (i.e. Powrhouse) a ‘merchant fee.’ In the vast majority of cases, the merchant then passes this on to the customer.

The merchant fee effectively increases the cost of the upgrade, which seems disingenuous. For example, the merchant fee might be 6.5%. So your $1,500 heat pump now becomes $1,600 but it’s marked as “interest free.”

Summary

Green Energy Loans are going to evolve, the market will continue to move. If you are considering a green energy loan now, we have shown that there are some fantastic products available.

But if you are not quite ready for an upgrade, it’s still worthwhile keeping these loans in mind. Shop around, keep your eyes peeled and take advantage of these incredible offers when the time suits.

Subscribe to Our

Subscribe to Our